Europe is currently in a serious debt crisis with a number of countries that are unable to repay their bonds and national debts that reach up to record levels. I consider there to be three key factors thanks to which Europe came to the current situation:

1. Imperfect political euro project

For some it may be just strong words, but hand on your heart, if someone asked you ten years ago: “What would you consider to be a failure of the whole euro project in 10 years?”, wouldn’t your answer resemble to what is currently happening in front of our eyes? The bursting bubbles in assets, bankrupting peripheral countries and the need to save Italy by printing of money by the “independent”European Central Bank (ECB)? This is not how success looks like.

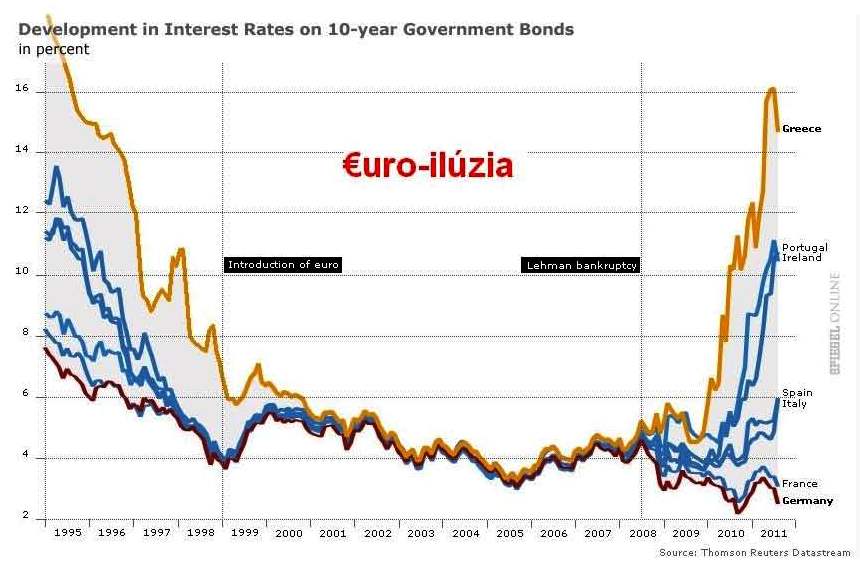

The core of the problem of the Euro-zone lies in the bad institutional settings. The stability and growth pact was only a pamphlet that was supposed to quieten the worries of the German voters about the fiscal incompetency of the Italians in the common currency union. Everyone ignored it. The ECB and the new euro, which it produced, became an unguarded common pasture that got used by anyone who needed. The amounts of new money radically lowered the costs of loans in the peripheral countries, where these unnaturally low interest rates blew giant bubbles whether it was in the real estates – Spain, Ireland, or in the government – Greece. The politicians supported this euro-illusion of the homogenous Europe and the financial markets believed it. Since the Greek bond was equally good for the ECB for the guarantee of new loans as the German one, the commercial banks didn’t have any reason to differentiate between them. Similarly as with Fannie Mae and Freddie Mac in the USA, there was an implicit guarantee coming from the strong member countries, that they won’t allow the bankruptcy of the peripheral countries. Today we see that the ones who bet on this guarantee were right.

The entrance of Slovakia to the currency union just before this organization started to change into a debt or transfer union has tragicomic features. Just look, whether you will find any threat of the need to provide a national guarantee exceeding 10% of the Slovak GDP for the bankrupting countries with an irresponsible fiscal policy in the risks of euro introduction, which were mentioned during a discussion about the right time of the entrance to the currency union. While the saved countries have a much higher life standard than ours. Also the threat of high interest rates to our national debt, in case we would end up behind the euro-door, is not appropriate. If we look at the development of the interest rates in the Czech republic, there is no aggravation of the expenses of their financing of the national debt compared to us. On the contrary, the interest rates of the national debt indicate that our membership in the Euro-zone after May 2010 after the creation of the Euro bail out funds causes more damage to us than good.

2. Reaction of Europe to the financial crisis

Besides that the financial crisis markedly lowered taxes and levy incomes of the countries due to the growth of unemployment and the reduction of revenue, the attitude of the politicians towards the finance sector contributed to the growth of the debts as well. During the crisis the politicians agreed that the banks have a special position in the economy and that’s why they cannot go bankrupt. When the banks came into bad times, after years of wealth and a risky management in the form of a massive utilization of the financial leverage and a low own capital, the politicians gave them public funds and socialized these losses – so they carried it over to the whole society. The losses of banks are gradually being transformed into a national debt and its repayment is now in the hands of the tax payers. It’s necessary to lower the pensions and to increase the taxes. It could have been different. The problematic banks could have been liquidated – their management sacked and assets overtaken by the country and sold to new investors. However this radical approach is, considering the close connection between the political class and financiers in Europe, unpopular and so today we have an unnecessarily big, hypertrophied bank sector, which is still not sufficiently capitalized and resembling a black hole sucks in the real resources from the tax payers and the productive section of the economy.

3. Expensive social systems that don’t correspond with the economical efficiency and demographic reality of the countries

For many years have the old member countries been managing with deficits, which are considered to be natural. It’s the doing of overly generous social systems that don’t correspond to the economical efficiency of the countries and demographic reality that lies in the aging of the population and a low birth rate. Abstinence of the will to reform these systems pushes the growth of the national debts and creates unbacked bonds of the systems.

Euro bailout funds – when the unsustainable debt is being resolved by another debt

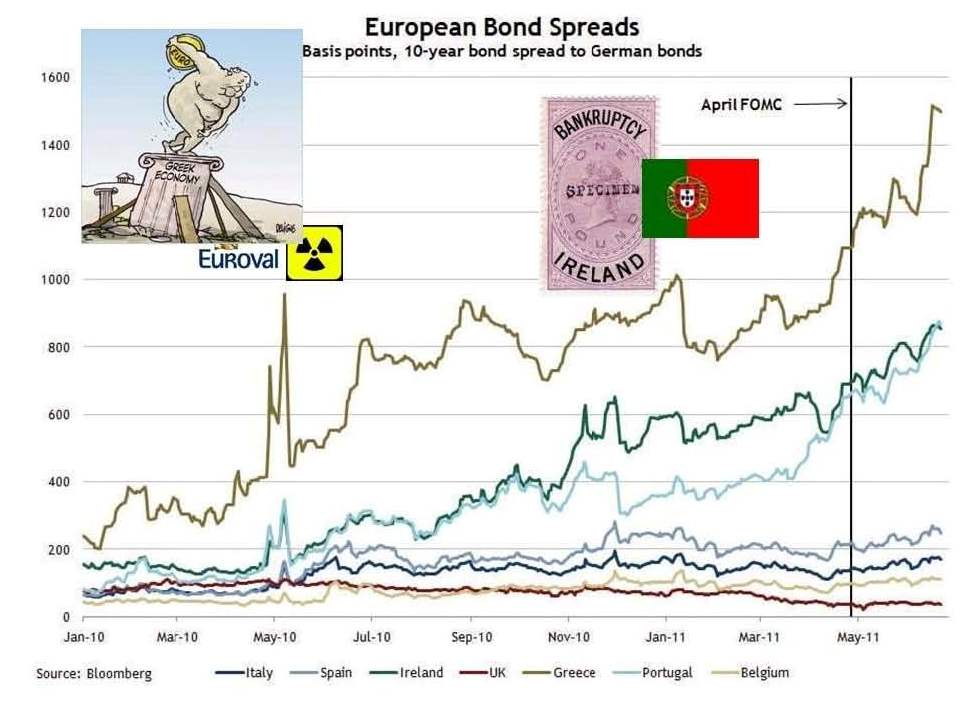

The money illusion, that we described closer in the earlier lecture, grew into reality, which was expressed as a global financial crisis. Suddenly there isn’t enough real capital to repay national debts, to continue a high consumption, generous Greek pensions or the repay of all mortgages in Ireland. The first problems will be visible in the weakest countries – countries with the highest debt and a tainted history of fiscal liability. Problems of the overly indebted Greece were started to be resolved by further loans. This is again another masked help to the bank sector. Because further loans won’t help the Greeks in a long term. It will only burden them more with debts. The banks in Europe have such a distinct status, that in order to protect them it came to a violation of the terms of the Treaty of Lisbon and the foundation of the Euro bailout funds.

This is a special Luxemburg corporation guaranteed by the countries of the Euro-zone, from which the money is lend to the problematic members. It’s a bad approach, that tries to solve insolvency- the inability to repay the debt of countries- by pretending that it’s a problem of liquidity- the short term insufficiency of liquid supplies for the repayment of debts. This approach only worsens the problems. Because the debt it still increasing and the problems are moved through the guarantee to countries that, up till now, didn’t need any help- for example Slovakia.

What were the main arguments, why was the Euro bailout fund created? Besides to prevent the bankruptcy of Greece it was supposed to serve to stop the spread of this problem to other countries PIGS (Portugal, Ireland, Greece, Spain). The results? Already after half a year there’s a need to save Ireland and Portugal! One year after the creation of the fund was Greece, even despite of the loan and a massive support from ECB, again on the verge of bankruptcy and requested more money. And the best part, this bad approach of moving of the debts of the problematic countries to others, relatively healthy countries, started to sink even the gigantic Italy in June 2011. And so it came to the worst case scenario. Not even the hard empirical disproof of the bad theories are enough for the politicians to leave this approach. On the contrary. At the beginning of summer it come to the increase of the Euro bailout funds, now it will be possible to recapitalize the banks with it and also give the banks in countries, that didn’t ask for help, direct loans and it will be possible to directly buy bonds from the bailout funds. Actually it is supposed to become a permanent form of the IMF (Monetary Fond) but before that the Treaty of Lisbon has to be altered.

Recommended bibliography

Rakúska teória hospodárskeho cyklu – Case Study Írsko

http://www.iness.sk/modules.php?name=News&file=article&sid=3036

Tragédia Eura

http://www.iness.sk/modules.php?name=News&file=article&sid=6296

Comments

4 comment(s). Display all comments.

Karpiš je ako obohratá platňa opakujúca tie isté kaleráby dokolečka. Najviac sa mi páči ten mravokárne poukazovanie na “nezodpovedný” západ žijúci si nad svoje pomery. No ono je to pravda, ale ak sa povie: A, tak je potrebné povedať aj: B. A síce že SR je svojím zameraním primárne exportná krajina, ktorá je ZÁVISLÁ na ochote “západu” sa zadĺžovať. Ešte komickejšia je kritika zahraničných bánk - matiek tých našich. Fugovanie bánk na SR v jasnej kartelovej únii ..však nikomu, ani Karpišovi neprekáža. V každom prípade Karpišové teórie sú presný obrazov nespoľahlivého partnera, ktorý podráža nohy, v tom najnevhodnejšom čase…

Na prvy pohlad velmi logicka uvaha.

Ale kde beries tu istotu, ze po zachrane bank znovu tieto banky nebudu zle investovat a ze ich po niekolkych rokoch nebudes musiet opat zachranovat?!?

Navyse si treba uvedomit, ze otvorenu ekonomiku zavislu od zapadnej Europy z nas urobil pan Miklos a jeho 19%-na dan. Je obsolutne nevyvazene, ze Slovensko ma produkciu 1mil aut rocne. Ak by sa totis v Europe uzavreli hranice z nejakeho dovodu, tak slovaci by po kratkom case nemali co jest, co si obliect, ale kazdy by vlastnil niekolko aut…

Vlada by mala jednoznacne zakazat vyrobu aut na tri smeny!!!

Ak spravne rozumiem slovu bankrot a v stave ohrozenia su nemecke, ale aj francuzske a atd. banky, ktore spravuju peniaze ludi v Zap. Europe, potom sa pytam, preco by sme tie banky mali nechat padnut a vypojili tak z hry spotrebu zapadu, ako hlavneho odbytista slovenskych vyrobkov? Nestupla by potom na SR nezamestnanost, kedze by nebolo pre koho vyrabat? A keby nebolo pracovnych prilezitosti, odkial by ludia vzali peniaze na splacanie vlastnych uverov? Nasledne by mali problemy aj SR banky atd. a dostali by sme sa na uroven depresiou zmietaneho Japonska. Myslim si, ze pomoct bankam, hoci su to obludy, je spravne. Alebo sa mylim…?

K tejto prednaske uz nie je co dodat. Zapadnej europe uz davno nejde o dobro nas vsetkych, ale su to len obycajni vychytralci a my by sme sa mali preto rychlo pobrat prec z eura, aj z Europskej unie aj z Nata.

Mimochodom preco pan Miklos nechal v 2000 zkrachovat Dopravnu banku? Nasu slovensku banku, ktora vykazovala velmi dobre vysledky? Robili tam nasi sikovni ludia, ktori riadili instituciu po svojom a nikto im nerozkazoval.

Viete aky nadherny pocit je to, ked si samy urcujete svoju pracu? Vacsina ludi dnes robi poskokov nemcom, vietnamcom, korejcanom atd. a vo vsetkych zahranicnych instituciach sa pracuje v neludskych podmienkach. Ja to nazyvam novodobe koncentracne tabory… Ale nasa pravica sa chvali tym, ze v Trnave aj v Ziline sa budu tahat nocne…

Zivot predsa nie je o peniazoch, ale o tom ci sa do prace tesite alebo nie. Tu je cosi z historie bankovnictva:

http://banky.sk/8014-sk/historia-bankovnictva-na-slovensku-iii.php